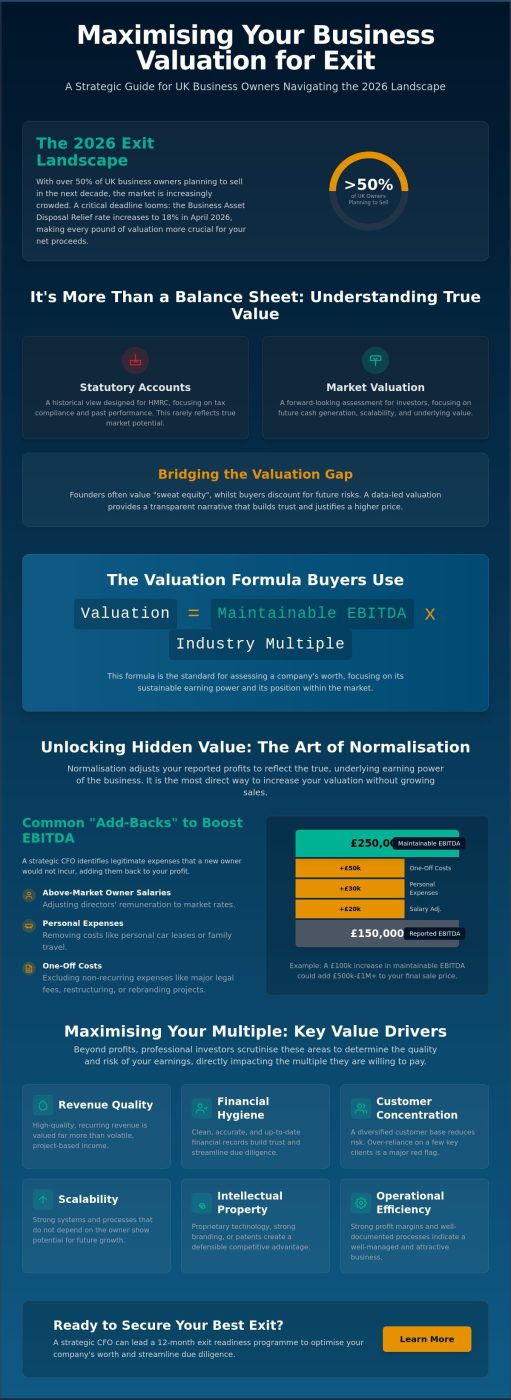

With more than 50% of UK business owners planning to sell their shareholdings over the next decade, the market is becoming increasingly crowded. Recent shifts, such as the Business Asset Disposal Relief rate increasing to 18% in April 2026, mean that a precise business valuation for exit is now more critical than ever for your net proceeds. It’s natural to feel a sense of unease regarding whether your internal expectations align with current market appetite, or to worry that your company might be undervalued during the rigours of due diligence.

We recognise that you’ve poured years of effort into your enterprise and deserve a result that reflects that dedication. This guide will help you discover how to accurately value your company and strategically optimise its worth to secure the highest possible sale price. You’ll gain a clear understanding of the EBITDA multiple method, alongside a practical checklist of value drivers designed to enhance your appeal to investors. By the end, you’ll have the clarity needed to navigate the 2026 exit landscape with confidence and strategic foresight.

Key Takeaways

- Learn how to determine a realistic business valuation for exit by selecting the appropriate methodology, ensuring your expectations align with current market appetite.

- Understand the “normalisation” process to adjust for one-off costs and personal expenses, presenting a clear picture of sustainable earnings to potential buyers.

- Identify the key value drivers, including revenue quality and financial hygiene, that professional investors use to justify a higher sale price.

- Discover how a strategic CFO can lead a 12-month exit readiness programme to optimise your company’s worth and streamline the due diligence process.

- Gain clarity on why your statutory accounts often fail to reflect true market value and how to bridge that gap to secure the best possible deal.

Understanding Business Valuation for Exit: More Than Just a Balance Sheet

In the current 2026 UK market, a business valuation for exit is no longer a static figure buried in a compliance report. It’s a dynamic assessment of your company’s ability to generate future cash under new ownership. Whilst your statutory accounts serve a vital purpose for HMRC, they rarely reflect the true market value of your enterprise. These documents are historical by design, focusing on past performance and asset depreciation. A buyer, however, isn’t purchasing your past; they’re investing in your future. With the Business Asset Disposal Relief rate now at 18%, every pound of valuation counts more than ever toward your final net proceeds.

Understanding the distinction between “Price” and “Value” is fundamental. Price is the final number on the sale contract, influenced by market sentiment and negotiation. Value is different. It’s the underlying worth based on risk, scalability, and intellectual property. To secure the best outcome, you must adopt the perspective of a sceptical investor. This psychological shift allows you to see your business as an asset to be optimised rather than a project you’ve built with “sweat equity”.

The Valuation Gap: Why Founders and Buyers Disagree

UK founders often overestimate their company’s worth by factoring in years of personal sacrifice. Buyers call this “emotional equity”, and they don’t pay for it. Instead, they apply discounts based on perceived future risks, such as customer concentration or reliance on the owner. You can bridge this gap by utilising various business valuation approaches to provide a transparent, data-led narrative. Clear financial reporting removes the guesswork and builds the trust necessary to sustain a high valuation during due diligence.

Valuation as a Strategic Roadmap for Growth

Performing a business valuation for exit early in your preparation cycle acts as a diagnostic tool. It highlights operational weaknesses, such as poor profit margins or inefficient processes, which you can fix long before reaching the market. By setting a “target valuation” for your desired exit date, you create a tangible goal for your leadership team. Engaging a finance director is essential during this phase. They provide the intellectual rigour needed to ensure your business trajectory aligns with your ultimate financial objectives.

The Mechanics of Valuation: EBITDA, Multiples, and the Art of Normalisation

EBITDA, which stands for Earnings Before Interest, Tax, Depreciation, and Amortisation, serves as the standard proxy for a company’s operating cash flow. It allows potential buyers to compare different businesses on a level playing field, regardless of their capital structure or tax position. However, the raw EBITDA figure found in your statutory accounts is rarely the number used for a business valuation for exit. To present your company in the best possible light, we must apply the art of normalisation.

Normalisation is the process of adjusting your reported profits to reflect the true, underlying earning power of the business under new ownership. It’s often the most efficient way to increase your exit price without the need for immediate sales growth. By identifying “add-backs”—expenses that are either discretionary or non-recurring—you effectively increase the base profit figure to which a market multiplier is applied. A standard accountant often focuses on tax minimisation, which can inadvertently depress your valuation. In contrast, an experienced CFO identifies adjustments that a buyer would accept as legitimate, such as excessive owner salaries, personal car leases, or one-off legal fees. Our exit strategy support ensures that every justifiable pound is added back to your bottom line, directly enhancing your final sale price.

What is Maintainable EBITDA?

Buyers are ultimately purchasing “maintainable” earnings. This requires removing “noise” from your profit and loss statement to show a sustainable trend. In the 2026 landscape, this involves carefully stripping out non-recurring recovery subsidies or post-Brexit grants that may have temporarily inflated recent figures. We look for a clean, repeatable profit level that a buyer can rely on. Common adjustments include:

- Removing one-off restructuring or rebranding costs.

- Adjusting director remuneration to a market-competitive rate.

- Eliminating discretionary spending, such as private club memberships or family travel.

- Normalising rent if the business operates from a property owned by the directors.

Decoding the Multiplier: Risk vs Reward

Once we’ve established a normalised EBITDA, we apply a sector-specific multiplier. In 2026, these multiples are influenced by UK interest rates and the record £190 billion in private equity “dry powder” currently seeking quality acquisitions. Smaller companies often face a “Small Company Discount” due to perceived risks like customer concentration. You can mitigate this by demonstrating robust management systems and a diversified revenue base. The multiplier serves as a definitive measure of the market’s confidence in your company’s future earnings potential.

Comparing Valuation Methodologies for UK SMEs

Choosing the right methodology is a strategic decision that depends on your industry, growth stage, and asset base. Whilst the EBITDA multiple method remains the predominant choice for most UK SMEs, a comprehensive business valuation for exit often employs a triangulation strategy. This involves looking at your company through different lenses to ensure no value is left on the table during negotiations. By comparing various approaches, you can identify the specific narrative that justifies the highest possible price for your unique circumstances.

Manufacturers or companies with significant property holdings often look toward asset-based valuations. This method calculates the net value of tangible assets, providing a floor price below which a sale would likely be illogical. For instance, maintaining the integrity of physical infrastructure through specialist contractors like Composites Construction UK can be vital for preserving this balance sheet value. Conversely, an entry valuation considers what it would cost a competitor to build your business from scratch, including software development, brand reputation, and customer acquisition. This “make versus buy” analysis can be a powerful negotiating lever when you are dealing with strategic acquirers who want to enter your market quickly.

In a similar vein, for office-based businesses, a professional refurbishment by Excel Business Environments Ltd ensures that the physical workspace is presented as a high-value, turnkey asset that supports the overall valuation narrative.

The Earnings Multiple Approach in Practice

Applying a sector average multiple to your normalised earnings is the most transparent way to reach a valuation. However, your business shouldn’t be constrained by a generic industry mean. Factors such as high recurring revenue, low customer churn, and a robust middle-management tier can push your multiple significantly above the industry average. For SaaS and subscription-based models, investors often look at the Rule of 40. This metric, which balances growth rate and profit margin, is a primary driver of valuation premiums in the tech sector. If your combined growth and margin exceed 40%, you’re in a strong position to demand a premium multiple from professional buyers.

When the DCF Method Trumps Multiples

The Discounted Cash Flow (DCF) method is often more appropriate for high-growth firms where historical performance doesn’t reflect future potential. It values a business based on the present value of its projected future cash flows. This approach requires meticulous strategic budgeting and forecasting to be credible. Buyers are naturally sceptical of “hockey stick” growth projections in DCF models. Without the backing of a seasoned CFO to validate the underlying assumptions, these models can easily be dismissed as over-optimistic. When presented with intellectual rigour, a DCF can justify a valuation that historical multiples simply cannot reach.

Maximising Your Sale Price: The Five Key Value Drivers Buyers Seek

A business valuation for exit isn’t just about calculating historical profits; it’s about proving the business can thrive without you. Buyers look for specific indicators that suggest a company is a safe, scalable investment. Whilst we’ve discussed the mechanics of normalising EBITDA in previous sections, these five value drivers are the levers that actually determine the multiplier applied to that figure. High-quality businesses focus on:

- Financial Hygiene: Clean, audit-ready management accounts reduce due diligence friction and build immediate trust.

- Revenue Quality: Recurring income is always valued higher than one-off transactional sales.

- Operational Scalability: A business that grows without a proportional increase in overheads is highly attractive to private equity.

- The “Bus Test”: If the business stops when the founder leaves, the value drops significantly.

- Market Position: Defensible moats, such as proprietary technology or strong brand loyalty, protect your future margins.

Reducing Founder Reliance

The “Founder Trap” is one of the most common reasons for a discounted multiple in the UK SME market. If you are the primary salesperson or the sole holder of technical knowledge, a buyer sees significant risk. Effective succession planning for founders involves building a second-tier management team that buyers can trust to lead after the sale. You should document every core process to ensure business continuity. When a buyer sees a company that runs like a well-oiled machine without the owner’s daily input, they’re more likely to pay a premium price.

Revenue Quality and Customer Concentration

A major threat to your business valuation for exit is the “80/20” risk, where a single client accounts for a massive portion of your turnover. This customer concentration creates buyer anxiety. If that client leaves, the business model collapses. You can mitigate this by transitioning from one-off projects to long-term service contracts. Presenting your client base as a diversified portfolio rather than a collection of fragile relationships is vital for a successful deal. We provide expert exit strategy support to help you restructure these revenue streams, ensuring your business is viewed as a resilient, high-value asset.

Preparing for Your Exit: The Strategic CFO’s Role in Value Optimisation

Strategic preparation is the final hurdle in securing a premium sale. A 12-month “Exit Readiness” programme provides the necessary runway to address operational gaps and maximise your business valuation for exit. For many UK SMEs, hiring a full-time CFO is an unnecessary expense when a fractional professional can deliver the same strategic impact. A part-time CFO offers the high-level expertise required for a transaction without the long-term overhead of a permanent executive salary.

During the sale process, your CFO acts as a vital shield against “price chipping.” This occurs when buyers attempt to renegotiate the headline price after discovering inconsistencies during due diligence. We bridge the gap between your compliance-focused accountant and your transaction-focused M&A lawyer. By maintaining a consistent financial narrative, we ensure that the value established at the start of the process is the value you receive at completion. We manage the data room and handle technical queries from the buyer’s team, allowing you to focus on running the business during a high-pressure period.

Cleaning the House: Pre-Exit Financial Audits

Identifying “skeletons in the closet” before a buyer finds them is essential for maintaining deal momentum. We conduct pre-exit financial audits to uncover issues with revenue recognition, tax compliance, or poorly documented contracts. We also focus on optimising working capital to ensure a “cash-free, debt-free” deal is as favourable as possible for the seller. A CFO-led audit can add 10-20% to the final valuation by removing uncertainty and providing buyers with a “clean” investment opportunity. This proactive approach ensures that you aren’t caught off guard by aggressive buyer accountants during the final stages of negotiation.

Partnering with PCFO for a Successful Sale

We act as your authoritative strategic partner, navigating the complexities of the UK exit landscape alongside you. Our approach to fractional CFO pricing UK is designed to deliver a clear return on investment by significantly enhancing your final sale proceeds. We don’t just report on your history; we future-proof your financial strategy to ensure your business valuation for exit reflects its true potential.

The first step toward a successful sale is understanding where you stand today. Booking an initial valuation and exit readiness health check allows us to identify the specific value drivers that will move the needle for your company. Let’s work together to ensure your years of hard work result in the highest possible reward.

Securing Your Financial Legacy in 2026

Achieving a premium business valuation for exit is the result of deliberate, strategic preparation rather than market timing alone. By normalising your EBITDA and addressing founder reliance early, you transform your company from a personal project into a high-value asset. We’ve explored how identifying specific value drivers and selecting the appropriate methodology creates a robust narrative that withstands the rigours of due diligence.

Our team of expert Finance Directors brings deep M&A experience to your boardroom, providing the composed, authoritative guidance needed to navigate complex negotiations. With a proven track record in UK SME exit optimisation, we act as your strategic partner to protect your net proceeds. It’s time to ensure your years of dedication result in the reward you deserve. Book your Strategic Exit Readiness Consultation with PCFO to begin your journey toward a successful sale. You’ve built a remarkable business; now let’s ensure your exit reflects its true worth.

Frequently Asked Questions

How long does a business valuation for exit take in the UK?

A comprehensive business valuation for exit typically takes between two and four weeks to complete. This timeframe allows for a deep dive into your management accounts, normalised EBITDA adjustments, and benchmarking against current market transactions. A rushed valuation often misses subtle value drivers that could significantly impact your final sale price. Taking this time ensures the final report is robust enough to withstand buyer scrutiny.

Will a buyer use my last year’s accounts or a three-year average?

Buyers typically look at a weighted average of your last three years of performance, with a heavier emphasis on the most recent twelve months. Whilst historical stability is reassuring, your current “run-rate” and future order book are often more influential in determining the final multiplier. They want to ensure the profit is sustainable and not a one-off peak before you exit the business.

Does my business valuation include the cash currently in the bank?

Most UK business sales are conducted on a “cash-free, debt-free” basis, meaning the cash in the bank is usually excluded from the headline valuation. You typically extract this cash before or at completion, provided the business retains enough working capital to operate. Debt is similarly deducted from the final price paid to the shareholders, ensuring the buyer starts with a neutral balance sheet.

How much does a professional business valuation cost for a UK SME?

The investment for a professional valuation varies depending on the complexity of your company and the level of detail required for the report. You should expect the fee to reflect the depth of analysis needed to support a high-stakes negotiation with professional investors. Rather than focusing on the initial outlay, consider the return on investment that a more robust, defensible valuation provides during price negotiations.

Can I value my business myself using an online calculator?

Online calculators are useful for a rough estimate but are inadequate for a strategic business valuation for exit. These tools cannot account for “soft” value drivers like management team strength, intellectual property, or customer concentration. A professional advisor provides the intellectual rigour and market context necessary to defend your price during the rigorous due diligence process that follows an offer.

What is a “good” EBITDA multiple for a UK business in 2026?

A “good” multiple in 2026 varies by sector, with many UK SMEs seeing ranges between 3x and 8x EBITDA. Service-based businesses might sit at the lower end, whilst high-growth tech or recurring revenue models can command significantly higher figures. Your goal is to move your business toward the upper quartile of your industry average by demonstrating low risk and high scalability to potential acquirers.

How does the current UK interest rate affect my company’s valuation?

Higher UK interest rates generally lead to lower valuation multiples as the cost of acquisition capital increases for buyers. When debt is more expensive, private equity firms and trade buyers must be more disciplined with their offers to maintain their target returns. This environment makes it even more important to demonstrate exceptional revenue quality and financial hygiene to offset these broader market pressures.

What happens if the buyer’s valuation is lower than mine?

If a buyer’s valuation is lower than yours, it often signals a gap in perceived risk or a misunderstanding of your normalised earnings. You can bridge this gap through structured negotiations, such as “earn-outs” where a portion of the price is paid based on future performance. Alternatively, you might choose to pause the process and spend twelve months fixing the specific value drivers the buyer highlighted.